![Business Structures as a Truck Driver [6 Types of Business Ownership]](https://blog.drive4ats.com/hubfs/Images/Blog/Business%20Structures/womandriverhangingoutwindowFeatured.png)

Ready to dive into truck ownership and running your own business?

That’s great news! You’re in a position that many drivers aspire to be in.

With the seat you’re sitting in, you have a lot of decisions to make. For starters, you need to think about how you’d like to operate your business. That means declaring a business structure and whether you plan to be a Limited Liability Company (LLC), an Incorporated, a Sole Proprietor, a Partnership or a Corporation. The choice you make affects how you run your daily operation, how you pay taxes and the overall cost of the business.

Are you confused yet?

That’s okay! This is confusing stuff. My day-to-day job as an operations support specialist involves a lot more than just money, so I’m here to help you make the right decisions to succeed out on the road and keep your business healthy.

Making a decision about how your business will operate plays a huge role in what you can and can’t claim on your taxes and which of your assets are and aren’t protected. If that still sounds pretty confusing to you, I promise that it won’t by the end of this article.

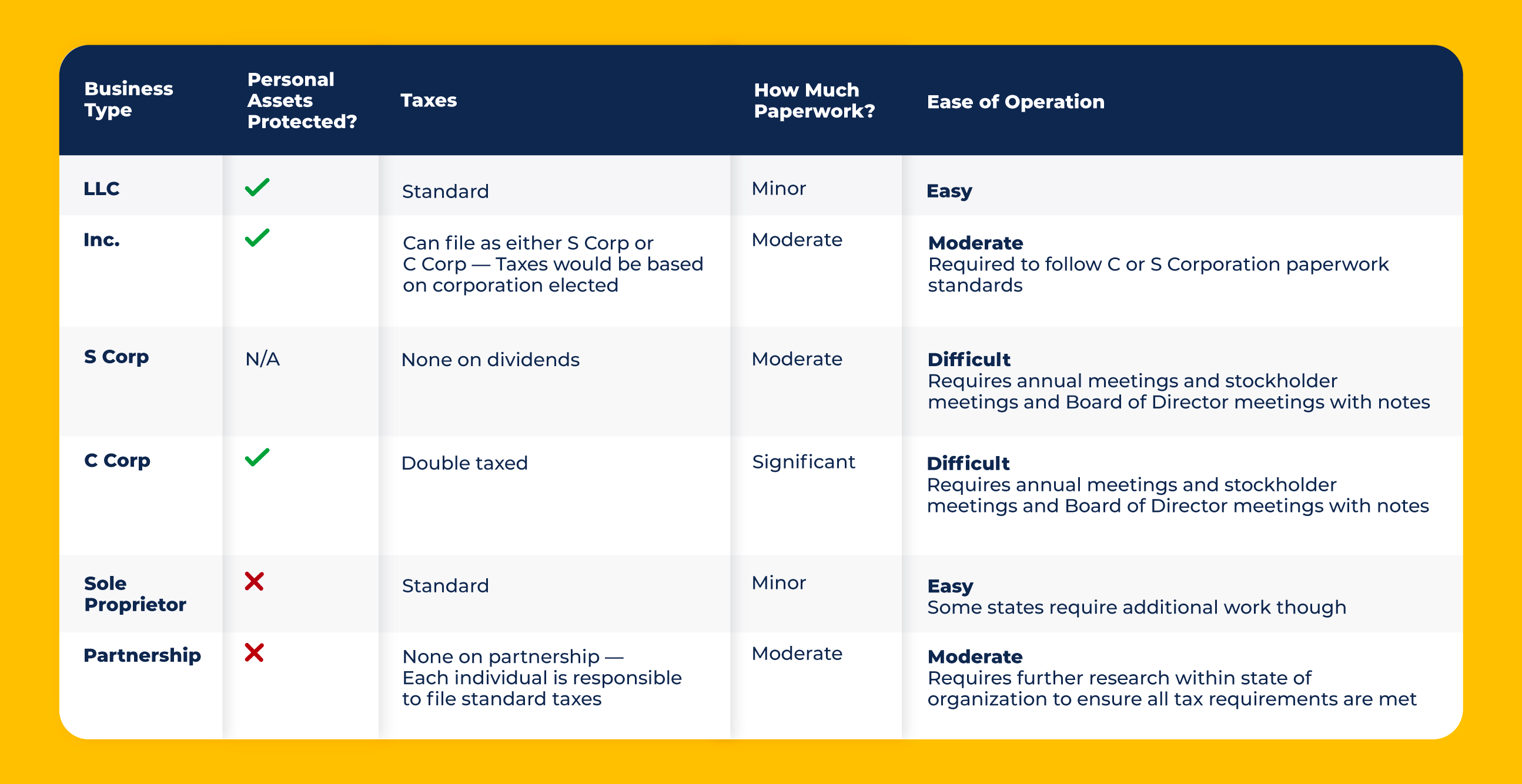

I’ll break it down into LLC, Inc., Sole Proprietorship, Partnership and S Corp and C Corp. Not only will I explain what each of them is and what it means for you as a driver, but I’ll also talk a little about the pros and cons of each. Stay tuned for a helpful chart you can use to make your decision.

LLC

A Limited Liability Company (LLC) is a business structure that’s allowed by state statute. Each state has different regulations you’ll need to be mindful of. Owners in the LLC are referred to as members.

An LLC is a legal entity. Within this, you may choose to identify as an S Corporation or a C Corporation.

Pros and Cons of an LLC

An LLC helps to protect all of your personal assets, meaning anything that you personally have purchased with either a line of credit using your social security number, your bank account or your credit card. Personal assets include your home, car, vehicles, jewelry — anything like that. This is a major pro of an LLC.

As far as the taxes go, it’s fairly standard and requires a lot less paperwork than other business structures. This is nice for drivers who want to avoid additional work in terms of tax preparation.

The primary con of an LLC is that all the profits are taxed. Any and all earnings the LLC earns will be taxed.

Another con is that if one member of the LLC leaves, the LLC is dissolved. For example, if a husband-wife team driving duo forms an LLC together and one of them decides to leave the LLC for any reason, the LLC will dissolve. The remaining spouse can’t remain part of the LLC.

Inc.

Inc. is short for incorporated in the business world. This means that the business structure is a legal corporation. Again, within this business structure, you can choose an S Corporation or a C Corporation as your tax designation.

An Inc. is similar to an LLC in that it’s a legal entity. You can also use an Inc. to blend together different business structures. For instance, two different sole proprietors or partnerships can come together to form a corporation.

Pros and Cons of an Inc.

Companies usually go incorporated to do things such as raising capital. A corporation is good for small business owners because it generally means they’re able to apply for small business loans, open a bank account and start building capital and credit under that business.

An LLC, on the other hand, is not going to be a relevant source to build a line of credit.

Sole Proprietorship

A sole proprietorship is an individual entrepreneurship or proprietorship. It’s a type of enterprise owned and run by one person. There’s no legal distinction between the owner and the business entity. This doesn’t mean, however, that the sole proprietor works alone. They may still employ other people.

If you never create or register a business, by default, you’re working and creating revenue as a sole proprietor.

Many lease drivers sign on as lease purchase drivers with a trucking company and start out as sole proprietors. It doesn’t require any paperwork or special tasks. A driver may, down the road, decide to change their business status and file for an LLC or Inc.

Pros and Cons of Sole Proprietorship

The great thing about a sole proprietorship is that there’s no work you have to do for it. You just need your social security number when you sign on with a company. There are no business documents or anything like that.

The major con is that there’s a huge risk of using the sole proprietor status if a driver were to ever be sued. Any and all personal assets you own would be at risk. That includes your house, personal vehicles, motorhomes and/or campers and other valuable items like jewelry. You may also be subject to wage garnishment.

Sometimes, for drivers working with a company, the company may take on some of that responsibility. But if they don’t and you’re being sued for a major accident, your personal assets are at risk. For example, you could lose your house.

The other thing with sole proprietors is that you're missing out on any and all business tax deductions that you could potentially receive if you ran under a different business structure. You also miss out on those protections that an LLC or an Inc. can give you in terms of your personal assets.

Partnership

A partnership is a relationship between two or more people to do business. Each partner contributes money, property and labor/skill. They each share the profits and losses.

A partnership is very similar to a sole proprietorship, but instead, it involves several owners instead of one. This is the default business structure for two or more owners that don’t register as an LLC, an Inc. or a C Corp.

Pros and Cons of a Partnership

Partnerships are beneficial because all parties are putting money and work into the business. All profits and losses are shared.

However, with a partnership, your personal assets aren’t protected. This is a major con. If the partnership were ever sued, your personal property, like your home, personal vehicle(s) and other expensive assets are at risk.

Without the legal entity within this partnership, I would also highly recommend what's called a partnership agreement. It’s a professional document outlining who is responsible for what at what time. For instance, partner A is paying these bills and partner B is paying these bills. Outlining these responsibilities in a partnership agreement means that their responsibilities can be upheld in a court of law if or when something tragic occurs.

S Corporation

An S Corporation (or S Corp) is a corporation that passes corporate income, losses, deductions and credits through to its shareholders. This is done for federal tax purposes.

An S Corp is technically not a business; it's actually a tax status. You may decide to form an LLC for a business structure and choose an S Corporation as your tax status.

Pros and Cons of an S Corp

With an S Corp, you’re not taxed on the dividends within your S Corp structure. In simple terms, dividends are whatever money is left over after the bills are paid. Let’s say you make $1,000 one week and $800 of it goes to your truck payment and other expenses. The remaining $200, your salary, is considered a dividend. You won’t be taxed on that $200 then. For many, this is considered a pro.

An S Corp is a federally recognized status, not a state-recognized status. That means you’ll more than likely need to file state taxes differently than you would file your federal taxes. Because this complicates the tax filing process, it’s highly recommended that you work with a certified public accountant (CPA) or a certified tax preparer. There are certain tax laws for state and federal that you’ll need to adhere to. Because extra work is required for tax preparation, this is a con of the S Corp.

Another con of the S Corp is that it can’t reinvest any profits. If your LLC with an S Corp designation is profiting, you can’t reinvest it for things like additional trucks, more equipment and the like. This is because you’re not taxed on your dividends. If you want to invest in new equipment, you’d need to take out a line of credit under the business.

S Corporations do require you to set up a payroll system. You have to document every time you pay yourself or you pay somebody else that’s associated with your business. Drivers should be doing this anyway.

C Corporation

A C Corporation (or C Corp) is a corporation taxed separately from its owners. This is its main distinguisher from an S Corporation (which does not separately tax owners). A C Corp falls under the U.S. federal income tax law.

A C Corp is a viable option but the likelihood of truck drivers using it is usually pretty slim. Most drivers would only pursue this option if they’re looking to build their own fleet, but even then, they’d probably look into starting a small business instead.

Pros and Cons of a C Corp

A C Corp is a legal entity and it has to pay double taxes. You have to pay taxes as a business and then you have to pay taxes personally.

The difference between S Corp and C Corp is that you can reinvest your profits with the C Corp. (But that’s because they're double taxed at the business level and employee level.)

Because of the double taxes, there’s a lot of paperwork and you’re probably going to need an accountant. To be successful as a C Corp, you have to be vigilant with your finances and have a good pulse on federal and state tax laws. It can be expensive to have an accountant regularly helping you with taxes and finances.

Also, you’ll need to have a board of directors and a yearly board of directors meeting to meet and go through finances and have official meeting minutes.

However, the C Corp does protect your personal assets, which is a major pro. You can also keep the profits in the business, which is good.

Additionally, your business will continue to exist without the original owners. So instead of like an LLC, where it will automatically dissolve if one of the members leaves, your C Corp will stay intact.

Making Your Decision

Deciding on a business structure isn’t an easy decision. In fact, you may still have some questions. Just like I would advise any ATS driver making a huge decision like this, I advise that you do your research, take your time with a decision and get a second or third opinion.

Carefully consider your choices and how they will impact how you operate your business, how much your business earns and how it will need to pay taxes.

First and foremost, ask yourself if you want your personal assets protected. That should guide your decision. Ask yourself whether or not you’re okay with putting your personal assets at risk — and remember, personal assets are seen (homes and cars) and unseen (retirement accounts).

Assess the risk in your moving forward to understand how to move forward. Understanding what you are and aren’t willing to risk is a great starting point and will guide your final decision about which business structure you’ll go with.

Sometimes tax professionals will try to sway you one way or another. Before you make that decision, take a close look at your finances and do the homework. That means researching each business structure, talking to other drivers and speaking to two or three CPAs or other tax professionals for a second opinion before you submit that paperwork. Set up meetings with a few CPAs in town, but I advise that you go to different, non-related businesses. For instance, don’t go to two different accountants at the same firm.

Talk to a Tax Professional

By now, you should have an idea of what direction you want to go in, or at the very least, a list of questions that you want to ask to further narrow down your choices.

I advise that you take your time making a decision. Carefully consider each option and write down a list of questions associated with each business structure. When you talk to a CPA or tax professional, carefully go down the list of questions and make sure you have an answer that makes sense to you before moving on. This is confusing stuff and your decision will have a huge impact on your future.

If you’re still new to navigating all this financial stuff and newfound responsibilities as a business owner, you can use all the help you can get. This article will help you with financial planning while this article will help you secure benefits.